The equimarginal principle is an important idea in the economic subfield of managerial economics. It is otherwise known as the “equal marginal principle” or the “principle of maximum satisfaction.” The equimarginal principle states that consumers choose combinations of various goods in order to achieve maximum total utility.

In other words, consumers will allocate spending their incomes across goods/services so that the marginal utility per dollar of expenditure on the final unit of each good purchased will be equal to all other goods purchased. It explains the way in which each consumer will spend portions of their income across a variety of different goods in such a way as to maximize their overall satisfaction.

The Equation for the Equal Marginal Principle

The equation for the equimarginal principle is as follows:

Marginal Utility of A Marginal Utility of B

————————————— = —————————————

Price of A Price of B

According to the equimarginal principle, when a consumer is making purchasing decisions, they will consider both the marginal utility (MU) of goods along with the price of goods. Taking both of these into consideration, they will make a decision that balances both. This means, in effect, evaluating the good’s MU/price—the marginal utility of expenditure on each unit of a good.

Equimarginal Principle Example

Let’s apply the equimarginal principle to a very simple case, with just two goods (socks and mittens). The price of each pair of socks, as well as each pair of mittens, is just $1. This means that the ideal quantity of goods to maximize utility would be 4. With a quantity of 4, 16/$1 is equal to 16/$1. See the table below for a representation of this example:

| Pairs of gloves/socks | Marginal utility of socks | Marginal utility of mittens |

|---|---|---|

| 1 | 40 | 22 |

| 2 | 32 | 20 |

| 3 | 24 | 18 |

| 4 | 16 | 16 |

| 5 | 8 | 14 |

Assumptions Underlying Marginal Utility Theory

Marginal utility theory rests on the assumption that consumers are always rational (a common assumption in the field of economics more generally), and that both the idea of utility and goods themselves can be quantified as specific units. It also assumes constant incomes and constant prices. In reality, things are a bit more complicated.

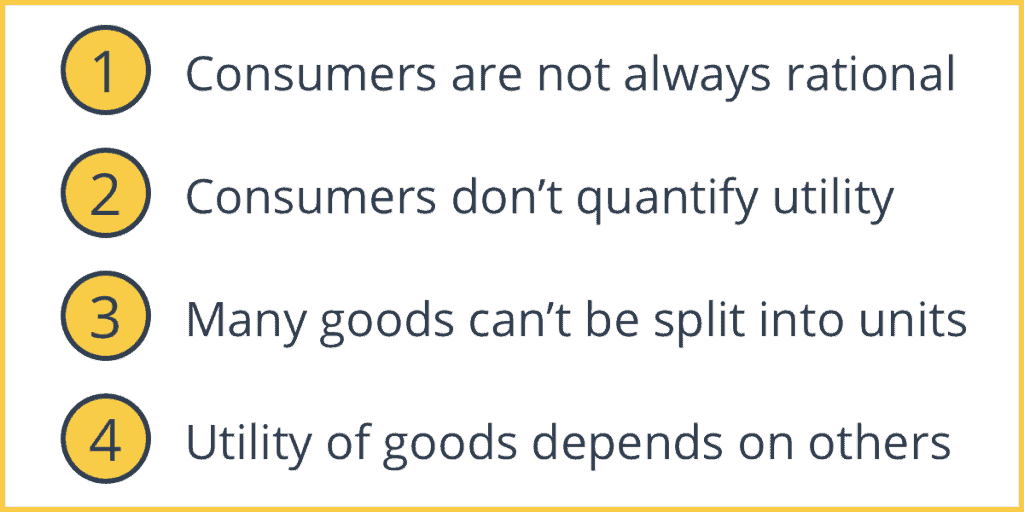

Limitations of the Equimarginal Principle and Marginal Utility Theory

Here are a few of the limitations of the equimarginal principle and of marginal utility theory as they operate in the real world:

1. Consumers are not always rational

Consumers will sometimes make economically irrational choices based on other reasons besides those that are quantifiable. Common influences outside of rationality include habits (people tend to repeat their purchasing habits once they’re satisfied with a good or service) as well as emotional impulses (which things like advertising or personal experience can influence).

2. Consumers do not typically quantify utility

In the real world, the concept of “utility” is likewise complex and difficult to quantify for most people. So when the average consumer is making purchasing decisions, they might have a general sense of the utility they will derive from a good, but are unlikely to quantify that level of utility. Assessing this can be even more difficult in light of how many products consumers have access to and the fluctuation of their income levels.

3. Many goods cannot be split into units

The equimarginal principle quantifies goods as units, but many goods cannot be divided into smaller units, and can only function as a whole.

4. The utility of some goods depends on other goods

When you buy a lamp, it has no real utility until you have also purchased light bulbs for it. That means that the utility of a lamp rests on having functional light bulbs and does not exist independently.