A Letter of credit is an obligation of a bank, usually irrevocable, issued on behalf of their customer and promising to pay a sum of money to a beneficiary upon the happening of a certain event or events.

Letters of credit are the substitution of the credit and good name of a bank for that of their customer, permitting the customer to do business with other individuals or firms on terms that otherwise might not be available to them. Letters of credit can be either domestic or international.

The Parties to the Transaction

A buyer that has committed in the sales contract to obtain a letter of credit begins by applying to its bank for a letter of credit to be issued “in favor of” or “for the benefit of” the seller. In this arrangement, the buyer is known as the account party, the buyer’s bank is the issuing bank or issuer, and the seller is called the beneficiary.

Documentary Letter of Credit Defined

The documentary letter of credit is defined as:

- The definite undertaking of a bank

- Issued in accordance with the instructions of their customer

- Addressed to, or in favor of, the beneficiary

- Wherein the bank promises to pay a certain sum of money in the stated currency

- Within the prescribed time limits

- Upon the complying presentation

- Of the required and conforming documents

Following A Letter of Credit Transaction

1. The Buyer’s Application and Contract with the Issuing Bank

Once the buyer has finalized a sales contract calling for payment to the seller under a letter of credit, it is up to the buyer to apply for that letter of credit at a bank. The application for the credit, usually done on the bank’s form and accompanied by an initial fee, contains the buyer’s instructions and conditions upon which the issuing bank may honor the seller’s documents.

The application will request the bank to issue a letter of credit to the seller promising to purchase the seller’s documents covering a certain quantity and description of the goods, with a value up to a certain amount of money, that are insured and shipped on or before a certain date.

The buyer may impose almost any conditions or requirements on the seller’s performance, as they pertain only to the seller’s performance. For example, the buyer could prohibit the bank from taking documents showing a partial shipment, or it could require a document that shows a specific method of shipping. However, the buyer must remember that this information is based on the buyer’s final agreement with the seller.

If the bank violates any terms of its contract with the buyer, then the buyer need not take the documents or reimburse the bank. For instance, if the buyer’s application requests the bank to issue a letter of credit calling for the seller to submit documents showing that it shipped “1,000 electric toasters”, and the bank, without approval, purchases documents showing that the seller shipped ‘1,000 toaster ovens,” then the bank is not entitled to reimbursement. The bank only deals with documents and money, not goods or inspection of goods.

2. Advising the Letter of Credit to the Beneficiary

The issuing bank will send the letter of credit to the seller via a foreign correspondent bank (a bank with whom the issuing bank has a reciprocal banking relationship) in the seller’s country. This bank is called the advising bank. An advising bank merely informs or “advises” the seller that the letter of credit is available to be picked up. The advising bank is not liable for the credit; it only provides the service of forwarding the letter of credit to the seller and checking the authenticity of the letter of credit.

3. Seller’s Compliance with Letter of Credit

The letter of credit tells the seller what it must do to be paid. It explains to him or her what to shop, how to ship, when to ship, and more. It contains specific terms and conditions drawn from the original sales contract and included in the letter of credit, such as the quantity and description of the goods, shipping dates, the type or amount of insurance, and so on.

For example, a buyer in California wants to import foreign-made beanbag chairs that must meet California’s strict flammability standards for upholstered furniture. The letter of credit might call for an inspection certificate to show that the chairs passed California’s standards.

The seller should inspect the letter of credit to see if it keeps up with the agreement with the buyer in the underlying contract of sale. The seller should examine other conditions of the credit to be sure that they can be met, such as can the seller acquire materials and manufacture on time for the shipment date? If the seller is unable to comply with the letter of credit for any reason, the buyer must be contacted, and an amended letter of credit can be issued.

4. Complying Presentation

A presentation is the delivery of the seller’s documents and drafts to the nominated bank or directly to the issuing bank. A complying presentation is one in which:

- The seller delivers all of the required documents

- Within the time allowed for presentation and before the expiry date of the credit

- Containing no discrepancies

- Which complies with all other terms of the letter of credit, the provisions of the UCP, and standard banking practices.

The nominated bank is that bank, usually in the seller’s country, that has been appointed or “nominated” by the issuing bank to honor the documents. The nominated bank is often the advising bank that originally transmitted the documents to the seller. If no bank is nominated, then the letter of credit is said to be “freely available” and can be negotiated through any bank of the seller’s choice.

5. Examination of Documents for Discrepancies

The UCP permits banks only to examine the documents “on their face” to see whether they comply with the letter of credit or whether there is a discrepancy. Banks may not look to any outside sources or conduct an independent investigation to see if the seller’s shipment to the buyer is in good order.

For example, a letter of credit calls for the shipment of “1,000 blood pressure monitoring kits.” The shipper’s invoice shows the sale and shipment of “1,000 sphygmomanometers and cuffs.” In this case, there is a discrepancy, and the documents will be rejected unless the buyer waives the discrepancy.

6. The Commercial Invoice

The commercial invoice is required by buyers, banks and customs authorities on every international sale. It need not be signed, notarized, or verified unless the credit requires. Where a commercial invoice is required, a preliminary “pro forma” invoice will not be accepted. The most important requirement is that the description of the goods in the commercial invoice must correspond to that in the credit.

7. The Ocean Bill of Lading

For transactions in which the letter of credit calls for presentment of an “onboard” bill of lading, the seller must present to the issuing bank a bill of lading showing the actual name of the ship, containing the notation “on board,” indicating that the goods have been loaded. Where the buyer and seller have agreed, and where it is approved in the letter of credit, it is acceptable for the bill of lading to show that the carrier has received the goods for shipment.

8. Certificated of Analysis or Inspection

Although these certificates are not required for the letter of credit transaction, sellers should ensure that certificates they include with their documents meet all the terms required by the letter of credit.

Other Types of Letter of Credit

A. Confirmed Letter of Credit

A confirmed letter of credit is one which a second bank, usually in the seller’s country, has agreed to purchase documents and honor drafts on the same terms as the original issuing bank. A letter of credit confirmed by a bank in the seller’s country will ensure prompt payment regardless of financial or political instability in the country where the issuing bank is located. However, a confirmed letter of credit is more expensive than an unconfirmed letter of credit.

B. Standby Letter of Credit

A standby letter of credit is one in which the issuer is obligated to pay a beneficiary upon the presentation of documents indicating a default by the account party in the payment of a debt or the performance of an obligation. A standby letter of credit is a backup payment mechanism that the parties hope they will never have to use. It can be used to guarantee performance under a service or construction contract, to guarantee repayment of a loan, or as security for almost any other type of contract.

Specialized Uses for Letter of Credit

A. Red Clauses in Credits

The red clause in credits is a financing tool for smaller sellers who need capital to produce the products to be shipped under a letter of credit. A red clause in a letter of credit is a promise by the issuing bank to reimburse the seller’s bank for loans made to the seller. The loan, then, is an advance on the credit. Loans can be used only for purchasing raw materials or for covering the costs of manufacturing or shipping of the goods described in the credit.

B. Revolving and Evergreen Credits

When a buyer is planning on regularly purchasing from a foreign seller, a revolving letter of credit may be used. Instead of having to use several different credits, one may be used with a maximum amount available during a specified period. As the draws against the credit are paid, the full amount becomes available again and continues until the expiration of the credit.

An evergreen clause in a letter of credit provides for automatic renewal of the letter of credit until the bank gives “clear and unequivocal” notice of its intent not to renew.

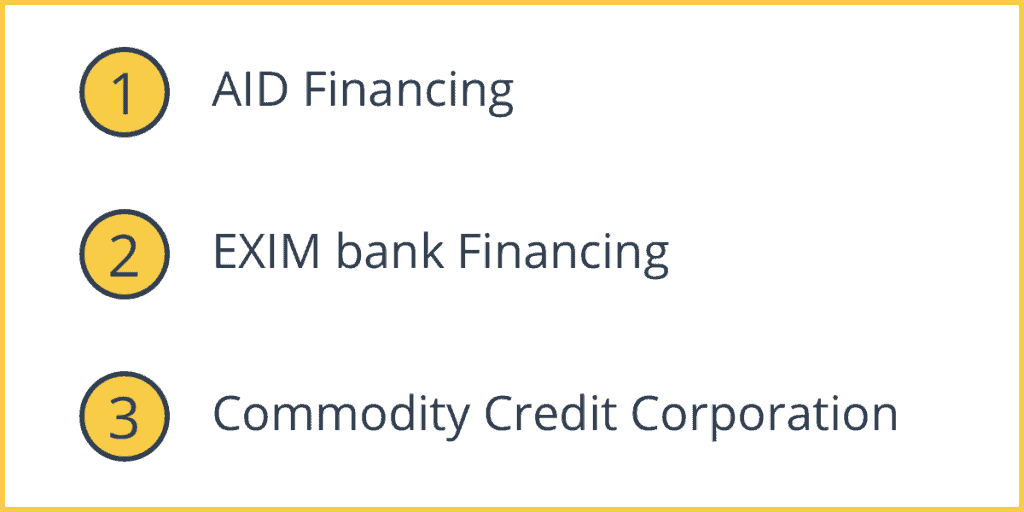

Some U.S. exports are financed by such agencies such as the Agency for International Development, the Commodity Credit Corporation and the Export-Import Bank of the United States. These agencies often insure payments made to U.S. sellers under letters of credit that are confirmed by U.S. banks using a letter of commitment from the agency to the issuing bank.

Examples of Letters of Credit in Trade Financing Programs

A. AID Financing

A typical AID financing situation might include a letter of credit. A country wishing to import U.S. products for developmental projects such as building roads, power-generating facilities applies to AID for financing. AID then issues its commitment to a U.S. bank that issues its letter of credit for the benefit of the U.S. supplier of eligible goods used in the project. The issuing bank receives reimbursement for payments under its letter of credit from AID.

B. EXIM bank Financing

EXIM bank is the most significant U.S. export financing agency. The bank can provide guarantees on loans made by commercial banks. They can also offer insurance on credit extended by U.S. exporters to their foreign customers. EXIM bank programs cover both the risk of nonpayment and political uncertainty.

C. Commodity Credit Corporation

The U.S. Department of Agriculture’s Commodity Credit Corporation provides payment assurances to U.S. sellers of surplus agricultural products to approved foreign buyers. Sellers often use standby letters of credit since they can draw under the credit for invoices that remain unpaid by the overseas buyer.

Law Applicable to Letters of Credit

A. The Uniform Customs and Practice for Documentary Credits

The Uniform Customs and Practice for Documentary Credits (UCP) is set of standardized rules for issuing and handling letters of credit, drafted and published by the International Chamber of Commerce with the assistance of the international banking community.

The UCP establishes the format for letters of credit, sets out rules by which banks process letters of credit transactions and defines the rights and responsibilities of all parties to the credit. Because banks were the main drafters of the UCP, its provisions tend to protect their rights in any transaction. The Uniform Commercial Code now defers to the UCP. As a result, the UCP has a far greater impact on the law of international letters of credit than does the Uniform Commercial Code.

B. Irrevocability of a Letter of Credit

Letters of credit issued under UCP 600 are presumed irrevocable unless clear language is used to make them revocable.

C. The Independence Principle of a Letter of Credit

The independence principle is a general rule of law that states that the letter of credit is independent of the sales contract between buyer and seller. Think of it as though the bank is purchasing documents for its customer. In UCP 600, Article 5 states “Banks deal with documents and not with goods.” Banks are neither concerned with the quality nor the condition of the goods.

D. The Rule of Strict Compliance

According to the rule of strict compliance, the terms of the documents presented to the issuing bank must strictly conform to the requirements of the letter of credit and the UCP. The thrust of the rule is that every provision of the bill of lading, invoice, insurance policy, and any other required shipping document must match the letter of credit. Even a small discrepancy can cause the bank to reject the documents. The reason for such a harsh rule is simple; it relieves bankers from the duty of interpreting the meaning of the discrepancy or its possible impact on their customer, and it relieves them of the liability of misinterpreting it.