Risk Mitigation

Ex-ante strategies prevent or reduce risk like savings. On the other hand ex-post or risk coping strategies mitigate the risk like dis-savings. These are two types of risk strategies for farmers to mitigate risk outcomes. Factors such as weather, rainfall, pests, and diseases hitting crops, irrigation can alleviate some income risk.

Aggregate shocks are problems that affect everyone in the village. They are not unique to just one farmer.

Idiosyncratic shocks are problems that affect only one farm.

Risk Strategies for Farmers

Farmers in developing nations often use these strategies to mitigate aggregate shocks and idiosyncratic risk.

1. Family

Family members can act as an insurance mechanism. Through transfers like borrowing money or seeds from family, which is an ex-post strategy to manage risk after the bad event happens. This strategy would also be good for aggregate shocks if they are spread out.

This situation is why marriage tends to occur outside the village to reduce the risk shock or have the son migrate to a city. These measures are ex-ante. However the transfers after would be ex-post.

2. Labor

Labor migration to other farms or villages can occur ex-post or ex-ante.

3. Savings

Savings (ex-ante) and dis-savings (ex-post). Farmers keep liquid assets that you can sell quickly. These include land, livestock, or jewelry.

4. Storage

Farmers often store crops to sell at a higher price (not at harvest time) (ex-ante).

5. Credit

Credits/loans from family or friends, traders (ex-ante or ex-post).

6. Diversify

Famers try to diversify production like by rotating crops or planting different varieties (ex-ante) or get into non-farm family businesses.

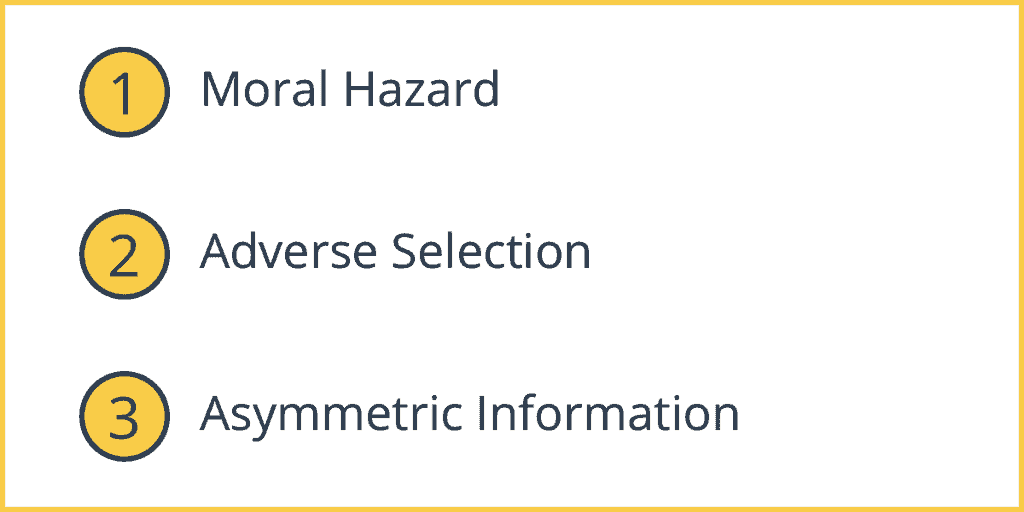

Problems with Private Insurance (To Mitigate Risk)

1. Moral Hazard

Moral hazard is knowing that you will be protected, so you have no incentive to manage risk. The farmer won’t engage in self-insurance.

2. Adverse Selection

Adverse selection means that the people who want to get insurance will be the people with high risk, but these people are the most costly to insure.

3. Asymmetric Information

The insurance company won’t have enough information on the farmer about things he could have done to minimize loss. This lack of information is called asymmetric information.

Within the family insurance system, there is no formal contract and information is more available. Family members are more likely to give a loan, since social threats of being excluded are useful.